The future of insurance/takaful claims is digital!

December 2, 2024

Did you know that most insurers/takaful operators in Malaysia offer some form of digital solution through their websites or mobile apps? Yes, that’s actually a fact, and it is through these digital ways that claimants can be alerted to updates instantly and have a better and more immediate view of the process.

Some insurers/takaful operators also have 24/7 road assistance service which enables their customers to contact the service centre at any time to receive help, assistance or towing of the damaged vehicle.

Not only that! Digital photographs of the loss or accident-damaged vehicle can also be sent via the same system. All these digitalisation enablers reduce the lifecycle of motor claims and make the approval process more efficient, which means that you can file a claim from the comfort of your home.

These initiatives are in line with Bank Negara Malaysia’s (BNM) call to improve motorists’ claims experience and outcomes, as set out in its Financial Sector Blueprint 2022-2026.

Imagine this—at the scene of an accident or vehicle breakdown, you could be exposed to questionable or even harmful practices. Unsolicited parties could show up at an accident scene to take advantage of accident victims by pressuring them to allow their vehicles to be towed away without notifying the relevant insurers/takaful operators, or deal with unknown parties to handle aspects of the claim. Victims may be made to pay unnecessary fees.

Damaged vehicles towed to unauthorised repairers also raise safety concerns from the use of non-genuine parts or sub-standard repairs. These practices contribute to greater risks of insurance/takaful fraud and exaggerated claims due to inflated costs of repairs and parts.

Additionally, manual claims processes have long turnaround times to approve and settle claims. Digital solutions like web or mobile apps can address many of these issues. By linking each party within the claims process, digitalisation can provide consumers with a more efficient and seamless experience.

It’s important that all insurance policyholder/certificate holders are aware and knowledgeable on the process of making insurance/takaful claims. The following guidelines will help make lodging a claim, a more convenient process.

The appointment of an adjuster will depend on the complexity of the case3

Quick claims guide for motor accidents. The 3 key steps are:

Contact your insurer/takaful operator immediately to notify them of the loss or damage. You can use the app, log in to their Claims Service Portal, or contact their hotline. If you’re not using the app, then the notification will come from the authorised repairer (unless it’s for windscreen reimbursement, which is usually done within a working day).

Date of loss/incident

Insured name/NRIC No/policy number

Contact number/e-mail address

Brief description of damage

Note: The required documents listed are not all-inclusive, as the need for additional information/document may become necessary during the claims process. Always keep the communications between yourself and your insurer/takaful operator open and cordial.

Source: Bank Negara Malaysia

Source: Bank Negara Malaysia

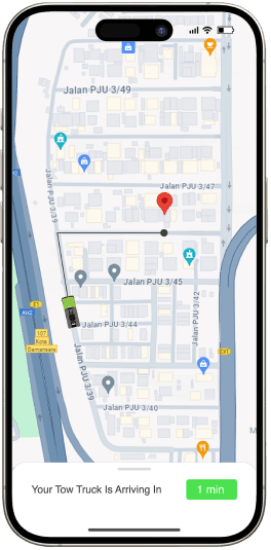

If you’re using your insurer’s or takaful operator’s digital roadside assistance app, here are the steps to file a claim.

Do not panic in the event of the accident or breakdown. Remember that the DRA is now a click or call away and touts do not have any rights to your vehicle. Capture photo and video evidence to support any investigation or claims.

Check for details of tow trucks (e.g. licence plate number) and keep track of their location and expected arrival time.

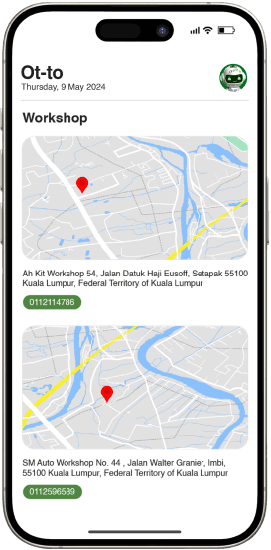

Inform your ITO or assistance provider about your workshop preference or select from the list of panel repairers.

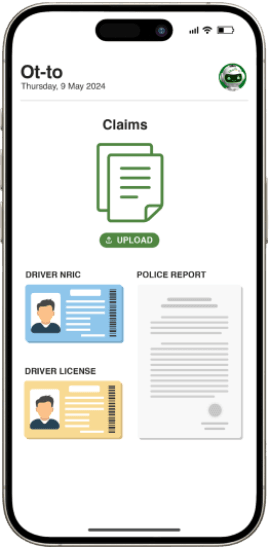

Log into your ITO’s website or mobile app to submit your claim documents.

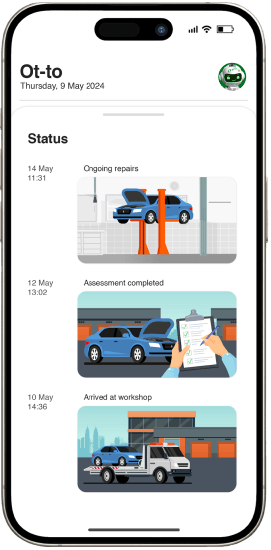

Repaired vehicle ready for pick up upon notification from your ITO or repairer.

Note: The above diagram is for illustration only. The actual user interface may vary across participating ITOs.

Source: Bank Negara Malaysia

Digital transformation is absolutely an enabler. The faster the motor insurance/takaful industry adapts to digital solutions, the better the outcomes will be. Motor claims of the future will be exciting, speedy, efficient, transparent, innovative, and digitally driven. Together with the friendly and helpful customer service support of insurers/takaful operators, the end-to-end claims experience will be brought to life!

This article is part of a ‘Jom, Level Up’ campaign under Phased Liberalisation 2.0, Consumer Education Programme (CEP), by Persatuan Insurans Am Malaysia (PIAM) and Malaysian Takaful Association (MTA).

Disclaimer: The information is provided for general information only. PIAM and MTA make no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.